This is why we save.

On Tuesdays and Thursdays, I post a picture and just a few words.

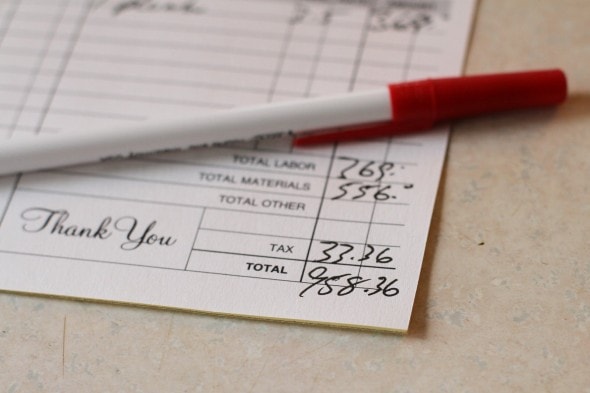

You know the plumbing problem we were having yesterday?

(Sewage was backing up through my shower drain.)

It turned out that the pump which moves water into our drain field had gone kaput. Dead as a doornail.

My brother-in-law says that car repairs somehow always end up being $1000, and maybe that's true for septic repairs too. 😉

Much as I would have preferred to spend this money on something more exciting, I'm thankful we had it in the bank. A $958 septic bill is a bummer, but it's not putting us into a state of financial panic.

No matter how little Mr. FG and I were making, we've always done our best to set a bit aside every month.

Because here's the thing about unexpected expenses:

You can pretty much always expect them to happen. You just don't know when.

Having a cushion in the bank makes it so much easier to weather these kinds of things, and the peace of mind that cushion brings makes all the frugal living totally worth it.

___________________

Here are more details about how manage our savings accounts, in case you were curious. An online bank and automatic monthly deductions are key for us!

___________________

We recently had to dip into our emergency fund when my daughter accidentally "opened" the garage door as my husband was driving into the garage. Not an expense we were happy about (when are you ever "happy" to pay for accidents, anyhow? LOL) but we were so glad that we had the funds. And, an honest repairman who was able to fix rather than replace the mangled door which saved us quite a bit.

Ouch! The joys of being a home-moaner.

An emergency fund is one of the most intelligent things people can do for themselves, financially speaking. It makes emergencies less stressful, at least I think so.

I'm trying to learn how to do some repairs myself but septic is one thing I'm just not touching. 😉

Yes! This was most definitely over our heads, both experience and equipment-wise.

Amen! While it is never fun to pay for these types of things, as you say, you can always expect unexpected events such as this. Living below your menas has such a huge payoff, if only people could see the positive side of it.

I'm glad everything is repaired, hopefully your life is back to normal.

Yes! Our toilets flush, our shower drains, and all is well. So. Very. Happy.

Ouch! Those repair bills just are not fun. And I'd say the septic and garage door repair are both best left to professionals. Those doors are dangerous because of the tension springs. Back when we were renters, our landlord sent her son to fix our broken garage door. He ended up in the emergency room with a bloody hand., it totally scared me to death( I heard yelling from the garage)but it could have been so much worse ( his face, for instance!)

And a professional did end up coming to fix the door. So one lesson is,

hire them to begin with on certain repairs.

Ouch! I do agree though, just recently my husband ended up needing a root canal and over $300 of it was not covered by out dental insurance it was nice to say "we will take it out of the emergency fund and pay it back".

Amen!

I'm so sorry to hear about this unexpected expense! I totally relate. Things like this sting, but so much less than if the money were not available to pay for them.

We also have a septic field, so I feel your pain! The year my daughter was born, we had planned on getting a new roof. Fortunately, we had an emergency fund, because not only did we re-roof our house, we also had to have a new drain field dug (not an easy feat in our back yard!) and our dishwasher decided to die on us. Is that a "trouble comes in threes" phenomenon? Glad to hear your plumbing problems are solved.

Ooh, what a rough year! I hope this isn't the first of three things for us.

I was thinking of this law of threes as I read down through the blog entry and the comments. I hope it's not the first of three things for you, too. Somehow it seems to happen that way around here...

We had to repair our septic system a few years back. It was sudden and unexpected. Like you, it wasn't what we would have chosen to spend the money on, but were we ever thankful when it happened that we could pay to have it fixed. Setting money aside when you can saves lots of stress later.

Yes, it was a tough year financially, but we weathered it. And if things would have been really bad, we would have done without the dishwasher (much as I hate the thought!). The other "expected-unexpected" expense that seems to pop up more frequently than I would like is dental emergencies. Our dental insurance isn't very good and it's sort of a shock how expensive crowns and root canals are. I think that "troubles in threes" is superstition ... but I think, Kristen, that your idea that unexpected expenses WILL happen and you need to have a cushion is SOOOOOO smart. Probably the hardest part is rebuilding that cushion once you have used it.

Calling these "unexpected expenses" is misleading. If you own a house, you know that things will break and maintenance will be required. You don't know exact timing or extent, but the eventuality is 100% certain. Therefore one should prepare in advance by saving now (if one can, of course).

OTOH I would consider a root canal to be a truly unexpected expense because they're not inevitable - many people go through their entire lives without needing one. In comparison, my teeth are weak so I need filling(s) every few years; *for me* it's an expected expence.

How about "expenses with unexpected timing"? 😉

I like that...a much broader category than what we have, kind of like "rainy day fund" 🙂

We don't currently have an emergency fund, because we're aggressively paying down our high-interest debt. We consider debt high interest if it costs us more in interest than our savings earn, which is 4%. Now that we've cut up our credit cards and mutually agreed to stop digging ourselves into the debt hole, it doesn't make sense for us to spend any extra money on interest when we aren't earning a comparable amount in savings.

If you have an emergency come up, how will you pay for it? Credit card? I'd highly recommend starting an Emergency Fund, while you're working at paying off your CC. Even if you just start small, it's better than nothing.

I definitely feel ya, Maggie--I am aggressively paying down my student loan debt, which, when I started, included loans at >8% (ugh). But like Shannon said, I have an emergency fund anyway, because otherwise when an emergency arises, you might be forced to take out a loan or put it on a CC with an interest rate much higher than your current debt. (Also totally jealous that your savings account pays 4%... is that a local bank?)

I'm in the process right now of identifying every expense we could possibly have and budgeting for them. I know I can't think of everything, but there is really no such thing as an "unexpected" expense - things break, accidents happen - so I'm going to try hard. 🙂

I can think of one truly unexpected expense- medical issues. In less than a year I went from being perfectly healthy to probably dying. They know what is wrong but it happened for no known reason. We had a large emergency fund and it is gone now but we are so lucky that we had it, we were able to pay for child care, tests, parking at the hospital, copays, specialists, etc... without huge amounts of concern. We have a very tight budget but we have no debt other than the mortgage even now. If we didn't have that money set aside when life was normal we would be in so much trouble right now.

All of our appliances seem to be going kaput all at once. I completely agree that it's a bummer to have to spend the money on something like that, but SO nice to not have to worry about racking up a credit card bill!

The thought of not having a cushion terrifies me. We've paid $5K in health insurance deductibles in the last six months and we have good health insurance and are healthy (one was me for my delivery and the other was when our baby got a fever--it was nothing). No wonder even people who have insurance have medical debt. Thank goodness we are savers.

This my be a bit personal, but I'm wondering what are some of the categories of saving people do other than your typical known monthly bills. And how much or what percentage of your take home pay do you save. I'm a single mom and carry all financial responsibility (never married, adopted my two kids as a single mom so no financial back-up from an ex spouse or anything like that). I'm pretty frugal but still find it a struggle, I have a very limited emergency fund. Right now I'm in the process of looking for a "new to me" car as my current car is on it's last leg and has some safety issues going on that really can't be fixed. Of course, I'm looking for something affordable and reliable and that I can fit into my budget, but will need to make monthly payment and not looking forward to that.

My goal has always been to have a savings account with enough money to cover 6 months worth of living expenses. It is only recently that I have been able to meet that goal. It's something to strive for, but for some people, realistically it's not going to happen overnight. Tracking spending and intentionally evaluating every purchase, and reading blogs like this for tips on frugality, can help to leave room in the budget to slowly but surely build up savings. As Maggie pointed out, sometimes it's a matter of balance. My husband totaled one of our cars last month after an incident with black ice. That meant that we had to dip into savings to by a new-to-us car. We also need a new roof this spring. After paying for the new roof, our emergency account will no longer be enough to cover 6 months of living expenses. If all goes well, we should have it fully funded again by September. My sister-in-law advised us to take out a car loan so our emergency account would remain fully funded. But as Maggie pointed out, the interest our savings account would earn would be less than the interest we would pay on the car loan, so we opted to pay cash for the car (and believe me, I know how lucky we are that we were able to do that). When the options are less than ideal, it's sometimes a matter of deciding which option is closest to the ideal.

I don't consider the question personal (unless you're asking how much I have in these accounts, in which case - tough luck!)

Most important is the Emergency Fund. That's for expenses that aren't predictable: losing my job, getting hit by a car. Standard suggestion is $1000 minimum, then in balance with paying other debt increase the emergency fund to 3-6 months' expenditures. This can vary, though: one self-employed friend keeps 2 years' expenditures on hand because his income is variable.

Next is the Life Happens Fund. This is for expenses that you know will happen but not necessarily when it'll happen. This includes new roofs and large car maintenance costs. How much this fund should be depends on how many of these expenses you have. I'm a car-owning home owner, so that's two expenses right there. Hard to say how much is enough - my feeling is that if I haven't spent money on my house recently, it's just saving up trouble for later and trouble = money.

Then comes predictable bills of known amount (mortgage, insurance, and so on) and unknown amount (electric, water). The former are child-simple to plug into a budget, the latter a little harder.

Then comes the rest: retirement, saving for a specific thing (vacation, pay cash for a new car, or whatever), general savings, etc.

The above funds are in order of priority (caveat: don't stiff the absolutely necessary current bills to create a savings fund).

The next question is, how to balance this with paying off existing debt. Here's my order of priority:

1. current bills: electric, water, mortgage, car payments, insurance (homeowner, personal, car, life), credit card minimums.

2. Emergency Fund: get to $1000 before any other savings. Once thit point is reached, proceed to step 3.

3. Emergency Fund + existing debt. Of the money I can save, put half to Emergency Fund and half to existing debt till Emergency Fund fully funded. I do highest interest rate first; others do smallest first. The 50/50 balance works for me but isn't universal. Once this point is reached, proceed to step 4.

4. Life Happens Fund + existing debt: Of the money I can save, put half to Life Happens Fund and half to existing debt until Life Happens Fund fully funded. Once this point is reached, proceed to step 5.

5. exsting debt. For some people, this is combined with saving for specific purchases; you decide what works for you. Once this is paid down, proceed to step 6.

6. Save for other things.

Any time you use a Fund, go back to the step to replenish that Fund.

The goals, in order of most immediate to longest term, are:

1. Have an Emergency Fund so you don't have to go further into debt.

2. Have a Life Happens Fund so you don't have to use the Emergency Fund.

3. Have enough savings that you don't have to use the Life Happens Fund.

This is why I'm a believer in a bigger EF than people like Dave Ramsey advocate. It's a good starting point if you have nothing, but a little larger cushion is exponentially better. When you're a "home-moaner" (Love this!),

1K can disappear in the blink of an eye, or in this case, the flush of a toilet.

Glad to know things are back to normal.

I couldn't agree more. Last year, I woke up to a 10' wide by 6'+ deep sink hole in our front yard caused by a leak in the sewer line. I fondly called it the money pit… Rest assured, $1000 didn't come close to filling that gaping hole. I am so glad had a substantial EF to fix this problem.

Holy moly! It didn't cost nearly that much when that happened to us. Of course Tom did it himself, buying the pump and installing it. Sorry we don't live closer. Mr.fix-it-himself-Tom could've done it for you for half that.

We had the same problem, it only cost us $160 which is not bad. The plumber said something blocking up and we thought maybe one of our girls (ages 2 & 3) flushed something (toy?) in the toilet. It's really nice to have emergency money for unexpected things like this.

I'm glad everything works well now with the problem you had. Cheers!

Amen! I couldn't agree more. In the past four months, our car needed a new battery and serpentine belt (regular maintenance, just unexpected timing). Then our refrigerator died right before Christmas (with a new one to the tune of $1000 out the door - and that was at a scratch and dent place!). Even though it was painful to write those checks, we had the money because we rarely eat out, don't have cable, buy mostly second hand clothes, drive older vehicles, avoid Target and the mall like the plague, cut my sons' hair myself (not that hard) and shop around for the very best deal - for items we truly NEED. As a result, we have plenty of money left over for when life happens 🙂

Ouch! Good for you having that in savings.

Our latest is an a/c leak... fortunately we discovered it near the end of the hot season so we've been able to put off replacing it and we've had time to get multiple estimates. (We have a choice of a 1K repair, a 3.5K replacement that will break even in energy costs in a couple of years, and a 5K total replacement that we don't need to do because the furnace is relatively new from the time the old one died and filled our house with smoke.)

Yes, leave the plumbing to the professionals! My brother-in-law is a plumber and half the calls he takes are related to people attempting to take on a project themselves!

And this is why my mother advised me to marry a plumber when I grew up. 🙂

Amen! I have an online savings account through a bank in Nebraska. I live in Michigan. I have a set amount direct deposited to my account. If I need to get at that money it takes three days to transfer to my checking account. I consciously made this a "process" to get at this money so we had an emergency fund. We have taken the course Financial Peace, Dave Ramsey through our church. We utilize the envelope system. We could become better at the budgeting this I will confess. However, even attempting is more than a lot of other individuals are doing.

Sorry to hear...but it is these unplanned events that come with home ownership is what lead our family to save for and maintain a "home maintenance and repair" sinking fund. Thankfully, with our sinking fund, these end up being more of an inconvenience than a financial burden.